- Differing assessments of the current business situation

- Only slight confidence in future prospects

- Investment climate clouds over

- Differing expectations for application industries

- Growth drivers show slight movements

- Composites index shows negative trend

For the 26th time, Composites Germany (www.composites-germany.de) has collected current key figures on the market for fiber-reinforced plastics. All member companies of the supporting associations of Composites Germany were surveyed: AVK and Composites United, as well as the associated partner VDMA.

In order to ensure that the different surveys could be easily compared, no fundamental changes were made to the questionnaire in this half-year period. Once again, the data collected was predominantly qualitative in nature and related to current and future market developments.

DIFFERENT ASSESSMENTS OF THE CURRENT BUSINESS SITUATION

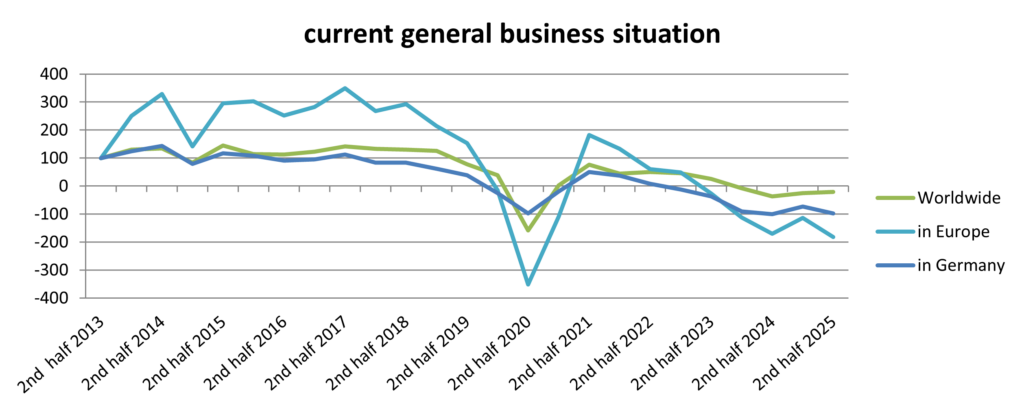

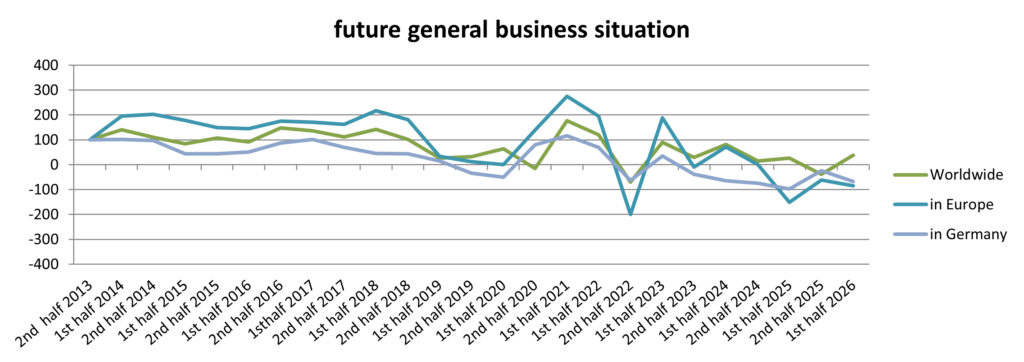

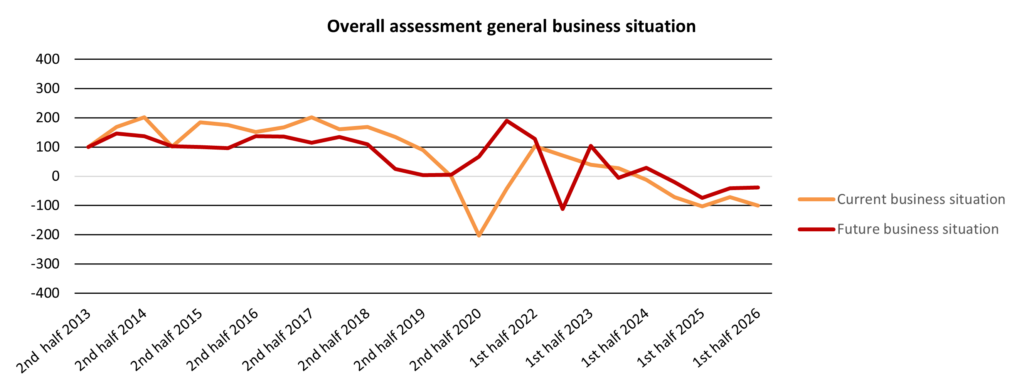

After the last survey showed a positive trend in the assessment of the general business situation for all regions surveyed, the picture has deteriorated again in the current survey. (See Fig. 1).

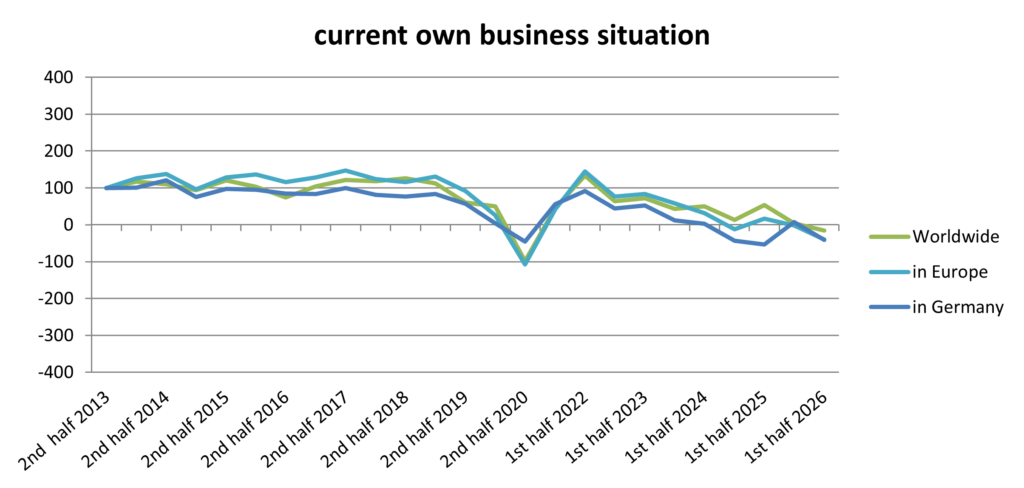

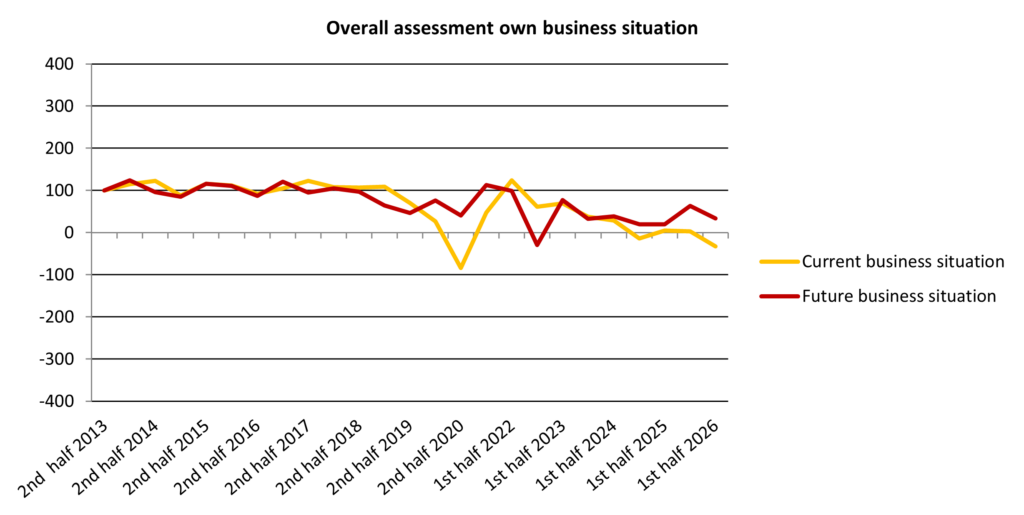

The assessment of the current general business situation for Europe and Germany has turned negative. Only the assessment of the global situation remains cautiously optimistic. The current assessment of the business situation is further weighed down by the fact that the participating companies view the situation of their own companies even more critically, with a negative assessment across all regions. (See Fig. 2)

These assessments are consistent with current surveys on the general development of the composites market in Europe. As a result of the coronavirus crisis, the market volume has declined by approximately 20 % since 2021. There are various reasons for this. On the one hand, there is increasing competition from non-European countries, especially Asia and the USA. In addition, formerly important export markets are increasingly being lost, which is due on the one hand to weaknesses in the respective domestic markets, but above all to the increasing supply of these markets by domestic production. Trade barriers, such as the current customs policy in the USA, are further exacerbating the situation. These challenges are accompanied by a general weakness in the industrial sector, with a significant exodus of industrial production from Europe. The continuing structural weaknesses in the main area of application, transport/automotive, are also having a significant impact.

So far, other areas of application, such as construction/infrastructure or electrical/electronics, have not been able to cushion the decline or support market volume.

The composites industry is heavily dependent on overall economic development, which is currently unsatisfactory in Europe and especially in Germany. Appropriate solutions that have already been initiated, such as the €500 billion special fund set up by the German federal government over twelve years for the modernization of infrastructure, climate protection, digitization, and education, are not yet having the desired positive effects.

It remains to be seen to what extent it will be possible to stop the current downward spiral through appropriate industrial support. There are still enormous opportunities, but these must be exploited along the entire value chain and with active industrial policy support.

FUTURE EXPECTATIONS WITH ONLY MODEST CONFIDENCE

At present, many of the companies involved do not seem to believe that the situation will improve in the short term, especially in Europe/Germany. The corresponding indicators are pointing downwards. In contrast, respondents expect the global situation to improve (see Fig. 3). However, it must be clearly emphasized here too that only around one in five expects improvement. Almost 80 % expect the business situation to remain the same or deteriorate.

INVESTMENT CLIMATE DETERIORATES

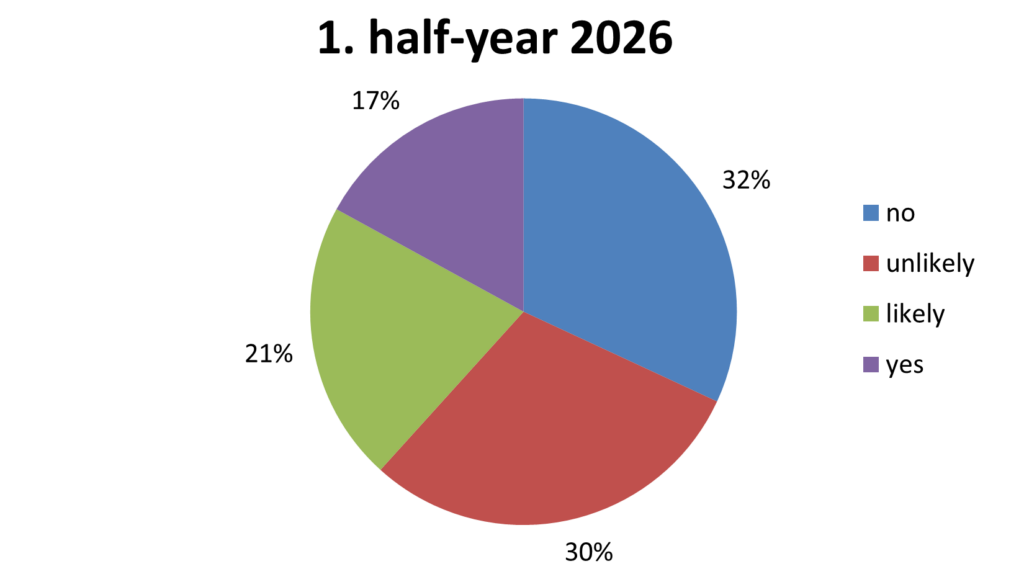

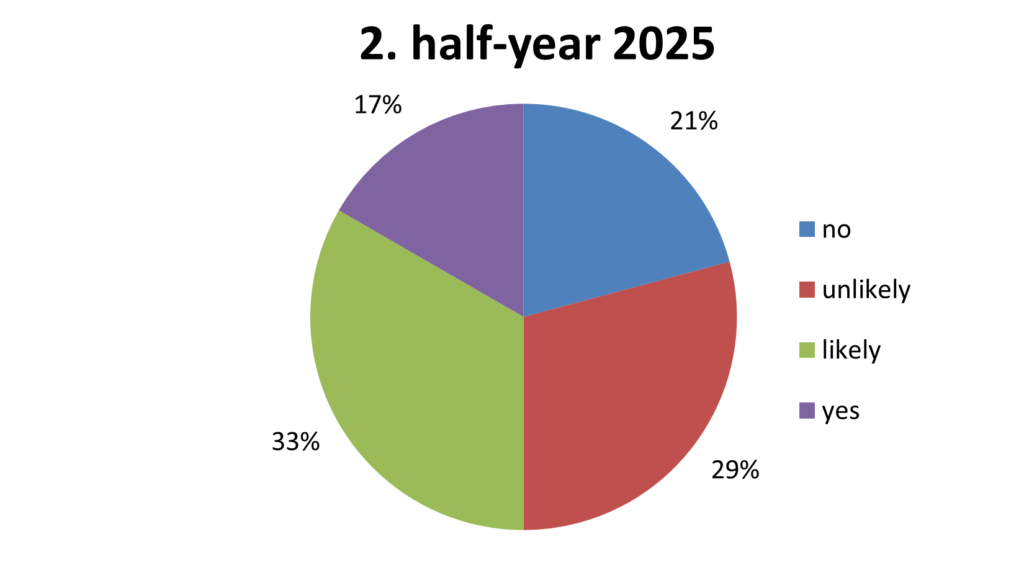

After the last survey in summer 2025 showed a positive impact on the investment climate, the indicators in the current survey have deteriorated. There are negative shifts in both personnel planning and planned investments in machinery and equipment.

The proportion of respondents who consider machinery investments likely or are planning them has fallen from 50 % (survey in the second half of 2025) to 38 % (see Fig. 4).

Figure 4: Assessment of machinery/equipment investments in the coming six months (100% missing data results from rounding inaccuracies)

The picture is mixed when it comes to personnel planning. Although the proportion of those planning to increase their workforce is rising from 15 % to 18 %, the proportion of those expecting to reduce their workforce is also rising from 27 % to 36 %.

Overall, more than one-third of respondents expect to increase their involvement in the composites sector, while only a fraction of respondents anticipate a decline in involvement.

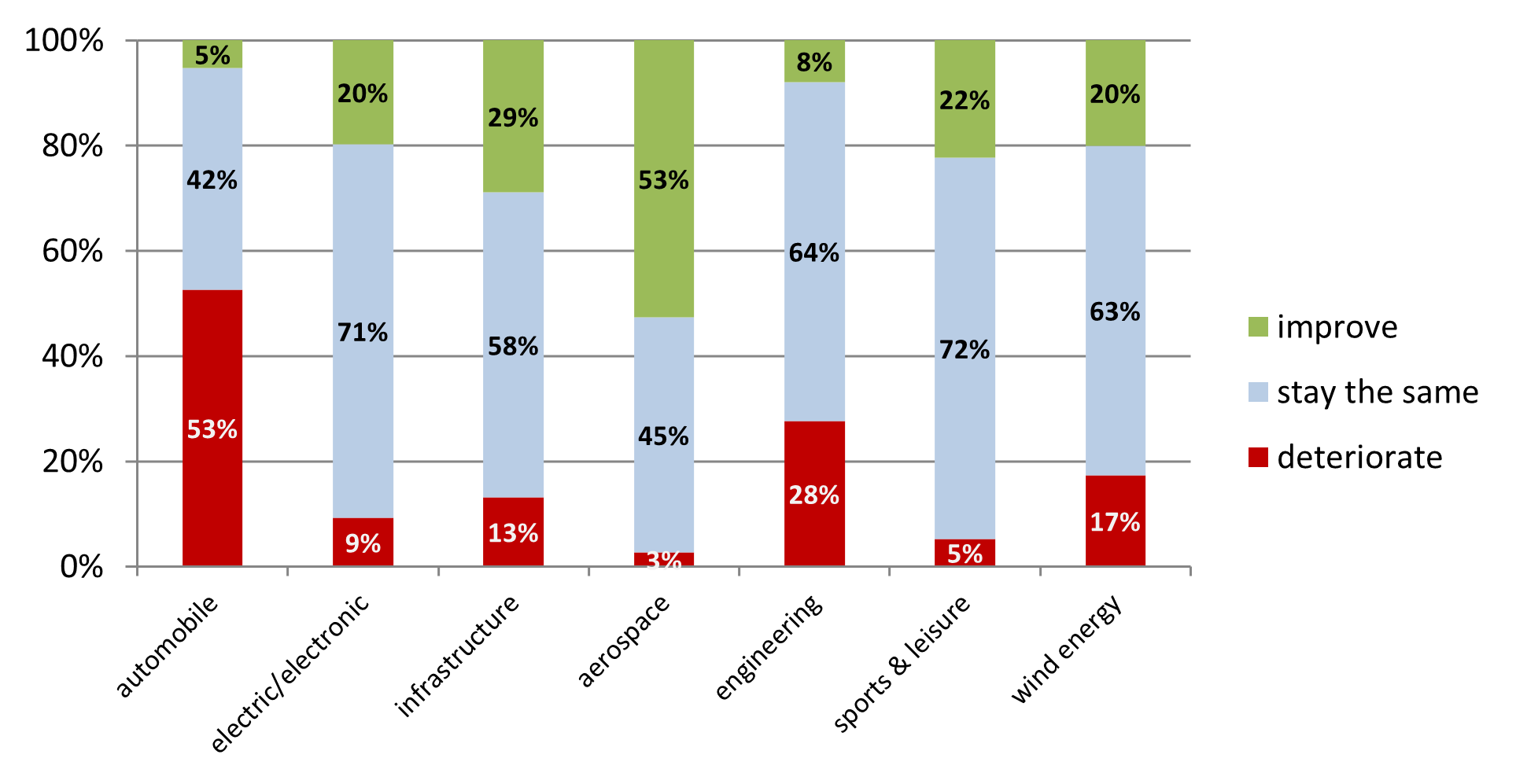

EXPECTATIONS OF APPLICATION INDUSTRIES VARY

The composites market is characterized by a high degree of heterogeneity in terms of both materials and applications. In the survey, participants were asked to give their assessment of market developments in various core areas. Their expectations vary greatly (see Fig. 5).

The most important area of application for composites is mobility. This sector is currently undergoing major upheaval and is in the midst of a massive crisis in Europe and Germany. This is also clearly reflected in the survey. Growth is expected primarily in the aviation and construction/infrastructure sectors. After four years of declining volumes, experts anticipate a recovery, particularly in the construction sector in Germany: “The German construction industry is facing a turnaround: after years of declining construction output, construction volume is expected to grow again in 2026 for the first time since 2020. According to the new construction volume calculation by the German Institute for Economic Research (DIW Berlin), construction volume is expected to increase by 1.7 percent in the current year and by 3.4 percent in 2027.“[1]

GROWTH DRIVERS WITH EASY MOVEMENTS

The current survey shows slight movement in terms of growth drivers. Regarding their assessment of which areas will provide the key growth drivers for the composites industry in the future, CFRP and GFRP are losing some of their influence as material systems in favor of a cross-material effect. Composites as a material group in general are increasingly being cited as growth drivers.

There is a slight shift at the regional level. The main growth momentum is increasingly expected to come from Asia. Germany is losing importance, while Europe is generally gaining slight popularity. The importance of North America as a growth driver remains virtually unchanged at a low level.

COMPOSITES INDEX WITH NEGATIVE TREND

After a positive sign in the last survey, the Composites Index is currently turning negative again in many areas. Only the assessment of the future general business situation remains slightly optimistic. (See Fig. 6).

Figure 6: Composites-Development-Index

Composites generally have excellent properties, which argues in favor of their increasing use in numerous application segments. Lightweight construction possibilities, corrosion resistance, freedom of design, and outstanding sustainability values are just a few examples that speak in favor of their use. Given the current negative economic and, above all, industrial development facing Europe, it is becoming increasingly difficult for the European composites market to hold its own.

It remains to be seen whether it will be possible to achieve a general reversal of this trend. Numerous political measures are currently being taken to strengthen the German/European economy. However, (financing) ideas and plans must then also be implemented. The construction/infrastructure sector in particular could receive significant impetus from the German growth package. Only by working together will it be possible to maintain and strengthen Germany as an economic/industrial location. Due to their special properties, composites as a material group in general continue to have very good opportunities to expand their market position in new as well as existing markets.

However, they remain dependent on overall economic developments.

The task now is to tap into new market segments through innovation, consistently exploit opportunities, and work together to further implement composites in existing markets. This can often be achieved more successfully through collaboration than alone. Composites Germany offers a wide range of opportunities thanks to its outstanding network.

The next composites market survey will be published in July 2026.

Press inquiries: Composites Germany, Dr. Elmar Witten (AVK)

+49 69 271077-0 | elmar.witten@composites-germany.org

About Composites Germany

The two strong organizations of the German lightweight construction/composite industry want to strengthen the German composites industry and research, define common positions and safe-guard overarching interests with the Composites Germany trade association.

AVK – Industrievereinigung Verstärkte Kunststoffe e. V. and CU – Composites United (as well as VDMA – Arbeitsgemeinschaft Hybride Leichtbau Technologien as an associated partner) are joining forces here with currently over 2,700 active member companies to promote the future topics of high-performance composites and automated production technologies in and for Ger-many.

Further information at: http://www.composites-germany.org

[1] DIW Berlin: https://www.diw.de/de/diw_01.c.996818.de/kehrtwende_am_bau__die_zeichen_stehen_wieder_auf_wachstum.html