Macro-economic developments are having a negative impact on the industry / Composites market is declining in Europe. The AVK – Industrievereinigung Verstärkte Kunststoffe – has published its annual market report for fibre reinforced plastics / composites.

Like all industries, the composite industry has been affected by strong negative forces in recent years. Like many sectors of the economy, the industry was hit particularly hard during the Covid pandemic. The war in Ukraine and sharp price increases for raw materials, energy and logistics subsequently had a highly negative impact on the economic climate, especially in 2022.

The world market for composites, on the other hand, showed an increase from 12.1 million tonnes to 12.7 million tonnes last year, amounting to around 5% growth. By comparison, European composites production in 2022 declined by 6.1%. Overall, market dynamics are currently accelerating, albeit in the face of many imponderables.

The AVK’s Market Report on Fibre-Reinforced Plastics and Composites 2022 sheds some light on developments, trends and challenges and provides a glimpse of the future.

You will find the full 2022 market report on the AVK website, at www.avk-tv.de.

The market under review

When considering glass fibre-reinforced plastics (GRP), this analysis covers all GRPs with a thermoset matrix. As before, NCFs (non-crimp fabrics) are reported separately. The thermoplastics market covers glass mat-reinforced thermoplastics (GMT), long fibre-reinforced thermoplastics (LFT) and continuous fibre-reinforced thermoplastics (CFRTP). One area that has been added since the last Market Report is an overview of the European production volume of short fibre-reinforced thermoplastics. Our overall review also includes the production volume of carbon fibre-reinforced plastics (CRP).

Overall development of the composite market

According to the latest figures from the JEC (www.jeccomposites.com), the volume of the global composites market in 2022 totalled 12.7 million tonnes. Compared with 2021, when the volume was 12.1 million tonnes, this was an increase of around 5%. By comparison, European composites production in 2022 declined by 6.1%. The overall European composites market thus went down from 2,962 kt in 2021 to 2,781 kilotonnes (kt), (see Fig. 1).

Europe’s share of the world market was therefore around 22%. America’s market share was on a similar scale. Asia’s global market share, on the other hand, was as high as 50%.

As in previous years, however, developments within Europe were not homogeneous. This is due to highly diverse regional core markets, substantial variability of the materials used, a broad spectrum of different manufacturing processes and widely differing areas of application. Accordingly, we can see different developments both regionally and, above all, with regard to different processes – although, in 2022, a decline could be observed in all regions and for nearly all processes. The only materials that saw growth were CFRTP and CRP.

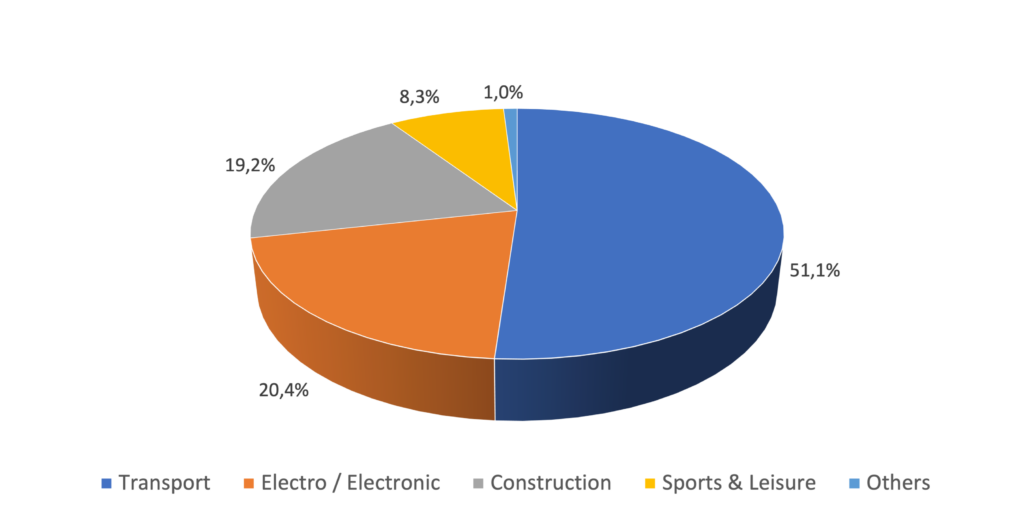

In terms of volume, the largest part of all composite production flowed into the transport sector, which continued to account for more than 50% of the market volume. The next two largest sectors were construction and infrastructure, on the one hand, and electrical and electronics, on the other. Transport includes the production of cars as well as commercial vehicles, aviation, public transport and many more. Construction and infrastructure covers, for example, pipelines, containers, tanks, structural sections, etc. The electrical and electronics sector, for instance, includes switches, housings, telecommunications equipment and control cabinets.

Development of the market for thermoset composites

The overall manufacturing volume of thermoset composites (excluding CRP) was 1,138 kilotonnes in 2022, compared with 1,250 kilotonnes in the previous year. Consequently, the share of this material group was 41.8% of the entire European market. As in 2021, unlike in thermoplastic systems, there was a slight 1.2% year-on-year downturn in the market share.

The two main areas of application for thermoset composites continued to be construction and infrastructure, on the one hand, and transport, on the other.

Whereas, until 2019, the transport sector had still been the largest application segment for the GRP industry (hereinafter this term will be used for all long and continuous fibre-reinforced thermoset and thermoplastic composites), there was a clearly increasing shift towards the construction and infrastructure sector in the year under review. This trend continued in 2022. By contrast, the thermoplastics market had been dominated for many years by applications in the transport sector, especially for cars and commercial vehicles.

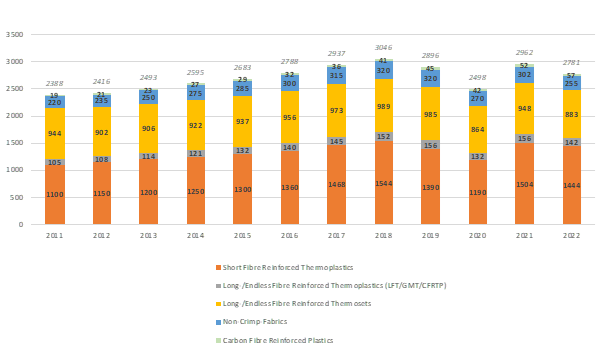

Market development for thermoplastic composites

The European thermoplastic composites market had a total volume of 1,586 kilotonnes in 2022, compared with 1,660 kilotonnes in the previous year (source: AMAC). Nevertheless, the decline was smaller than for thermoset systems. The share of these systems in the overall European market rose from 57% in 2021 to 58.2% in 2022. The largest material group within thermoplastic composites and also in the market as a whole was short fibre-reinforced plastics.

The main area of application for thermoplastic composites was the transport sector, which accounted for over two thirds of the market. This segment was dominated by cars and commercial vehicles. Together with applications in the electrical and electronics sector, the 2022 market share was 90%. Since the beginning of the survey in 2011 and despite the many challenges, the overall market segment grew by more than 30%. What is striking in this context is the strong increase within this market segment despite a sharp decline in car registrations. In many cases, production and thus sales of volume models were cut back in favour of high-margin models with higher prices. A similar picture emerged for commercial vehicles in 2022.

The strong increase in thermoplastic composites over the past few years and their relatively small decline in 2022 can therefore only be explained by an increased use of composites in this segment. In addition to making changes to designs and converting components and component groups, another option is to substitute more existing materials with composites.

Development tendencies of processes/parts

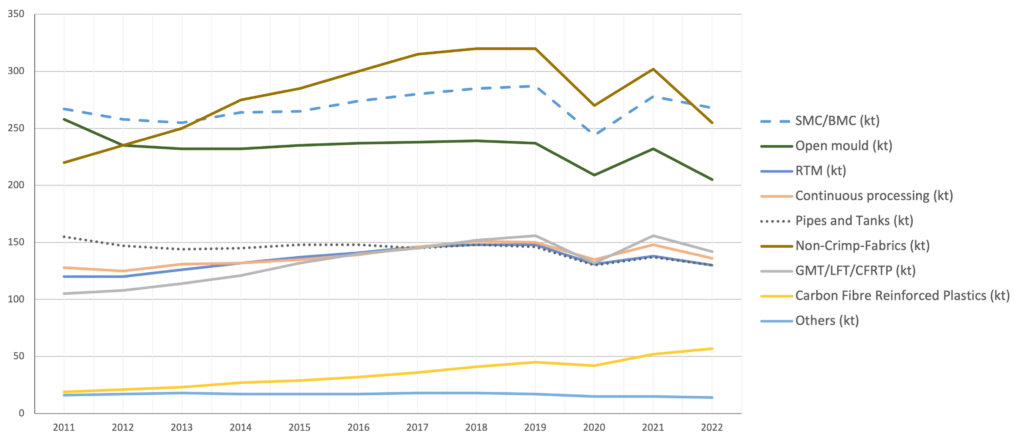

When looking at the quantitative developments of the main processes and parts of composite production, the individual segments cannot always be distinguished very consistently or clearly. The material properties of short fibre-reinforced materials sometimes differ significantly from long and continuous fibre-reinforced systems. The glass fibres within the material are usually less than 2 mm in length. Yet they do increase the level of properties compared with non-reinforced materials. Generally speaking, materials are distinguished with regard to their basic and, in some cases, clearly different mechanical properties. The CRP figures are also included here.

The largest single segment since 2014 has been non-crimp fabrics (NCF). 2022, however, was the first time that SMC and BMC materials were the largest material group, many of which were used in large series applications. The third place was occupied by open mould processes, which are often applied in highly manual contexts. In terms of volume, the other processes mentioned here were on a very similar level. In particular, we can see above-average growth in CRP – at a lower absolute level – especially in the year under review.

Regional market developments

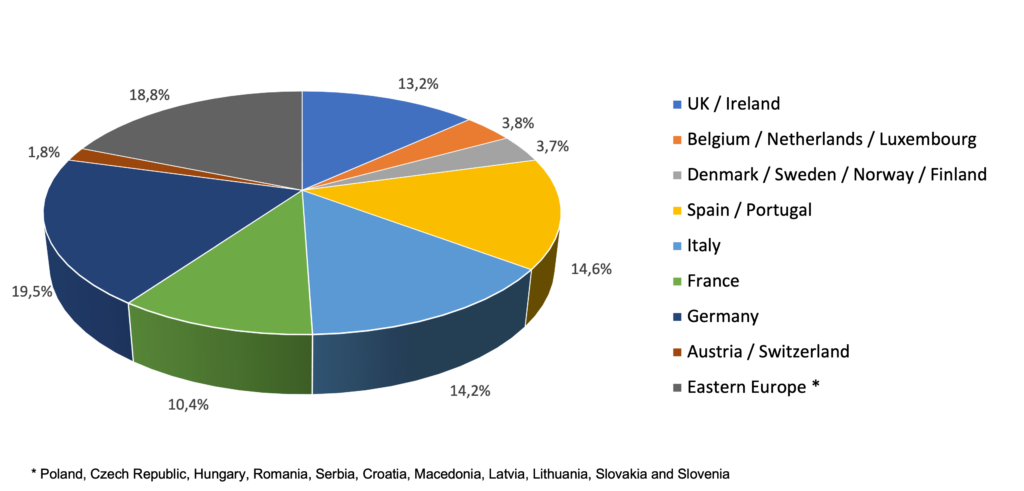

The underlying data covers all long and continuous fibre-reinforced thermoset materials. Thermoplastics are not included in the regional analysis, as there is currently no regional breakdown of these quantities of materials. The percentage distribution by regional core areas has hardly changed at all between 2021 and 2022. The German thermoset market reached a volume of 222 kt in 2022. As in previous surveys, Germany was the largest market in the regions covered, representing 19.5% of the total.

Second place was taken by the Eastern European countries with a market share of 18.8% and a volume of 214 kt. Spain and Portugal formed the third largest group, with a processing volume of 166 kt and a market share of 14.6%. Italy followed closely behind Spain and Portugal, with a market share of 14.2% and a composites processing volume of 162 kt. Taken together, the four regions represented two thirds of the European composites market. The second biggest processing region within Europe was the UK and Ireland with a market share of 13.2% and a volume of 150 kt. France was a long way behind, with a market share of 10.4% and a production volume of 118 kt.

In addition to this purely volume-based perspective, it must always be borne in mind that nearly all regions had very different areas of emphasis in their composites industries. As a result, each country or region was often affected by macro-economic developments in a completely different way. A pan-European view can therefore only ever provide a rough indication of the development.

Other composite materials: CRP and NFRP

In addition to the material groups discussed so far, carbon fibre-reinforced plastics (CRP) and natural fibre-reinforced plastics (NRP) are the most important ones in terms of volume. The CRP market volume developed highly dynamically in 2022, achieving 9.6% growth compared with 2021. The overall volume in Europe rose to 57,000 tonnes.

No new information is currently available for NRP.

Outlook: The future is looking bright for composites.

How will the composites market develop in the medium and long term? Over the last few years, markets have been changing at an increasingly rapid pace.

The two central areas of application for composites are construction and infrastructure, on the one hand, and transport, on the other. Both areas also have a major impact on the wider economy, which – due to the interdependencies mentioned above – often develops in parallel. This wider economy has been and is still being shaken by several severe crises. In particular, it has been weakened by the Covid pandemic and other negative factors such as the war in Ukraine – factors which are continuing to cause major potential insecurities.

The manufacturing sector, which includes the production of composite components, has traditionally been more important in Germany than in the other large economies of the EU. This makes Germany’s economy particularly dependent on the industry.

We cannot currently provide any reliable quantitative forecast of the development of production volumes in composites within the various regions and manufacturing sectors. One key indicator for assessing the situation from a manufacturer’s perspective is the Producer Price Index. This index measures the price changes of commercial products manufactured and sold within a given country. It illustrates the magnitude of price increases in recent years.

A detailed analysis of contributing factors shows that the main driver of the enormous increase has been, above all, a massive rise in energy prices. The strong rise in the cost of production in the most important European national economies seems to have stopped for the time being, and the relevant indicators are currently beginning to come down. However, the resulting price reductions – measured in terms of short-term purchase values on the stock exchanges – might still be significantly lower. The future still holds plenty of potential for price drops.

In addition to manufacturing costs, another extremely important element in the highly internationalised composites market is the cost of logistics. Here, too, some of the costs have fallen sharply. After increasing almost tenfold during 2021, container freight rates have now returned to pre-crisis levels.

Despite the latent danger of a global recession, the above indicators currently suggest that markets are calming down. For example, the GfK Consumer Climate Index, which measures the level of income and consumer confidence for the next 12 months, has edged up a little in recent months, after its historic low in October 2022 (-42.8 points), so that it is now at -30.5 points.

For the composites industry, the two most important purchasers are the transport sector and the infrastructure and construction sector. Taken together, these two areas account for more than 70% of the market volume. However, developments in these core markets were very different.

We already mentioned the sharp drop in new car and commercial vehicle registrations in 2022, resulting in the lowest value for 30 years. The construction sector, as the second largest application segment, often proved to be robust during the crisis, although there has been a slight decline in construction activity in recent months.

Another reason for optimism is the employment situation, which also has a significant impact on private consumer spending. In early 2023, the average unemployment rate in the EU was lower than it had been for many years.

Despite the challenges mentioned above, composites are set up for success in the future. There is much to suggest that the fundamentally positive developments of the last few years will continue. In the medium term, structural changes in the transport sector will open up numerous opportunities for composites to gain a new foothold in new applications. Major opportunities can also be seen in construction and infrastructure, an area where composites offer enormous hope due to their unique level of properties that predestine them for long-term use. The main assets of these materials in terms of application are clearly their durability, their almost maintenance-free use, their potential for use in lightweight construction and their frequently positive impact on sustainability.

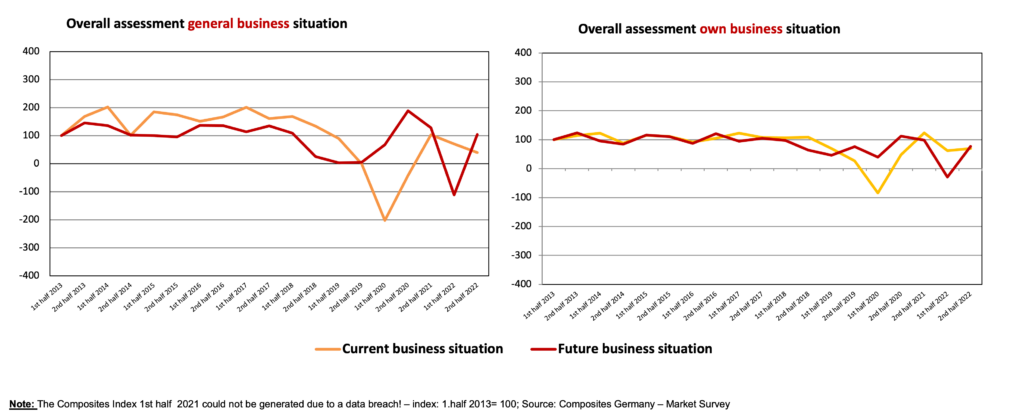

This is also the view of the composites industry itself. To compile the Composites Index at six-month intervals, Composites Germany takes a survey among all member companies of the umbrella organisations of Composites Germany (AVK, Composites United and the associate partner VDMA), asking each of them to provide a qualitative assessment of the market. Whereas companies are currently taking a critical view of today’s economic situation, their expectations for the future are clearly becoming more positive.

More detailed information as well as additional graphics can be found on the AVK website at www.avk-tv.de.

Press enquiries: Birgit Förster, Tel. +49 69 271077-13, birgit.foerster@avk-tv.de