- Critical assessment of the current business situation

- Future expectations deteriorate

- Investment climate remains subdued

- Expectations for application industries vary

- Growth drivers with little movement

- Composites index points downwards

For the 23rd time, Composites Germany (www.composites-germany.de) has collected current key figures on the market for fiber-reinforced plastics. All member companies of the supporting associations of Composites Germany: AVK and Composites United as well as the associated partner VDMA were surveyed.

In order to ensure that the different surveys can be compared without any problems, no fundamental changes were made to the survey this half-year. Once again, mainly quali-tative data was collected in relation to current and future market developments.

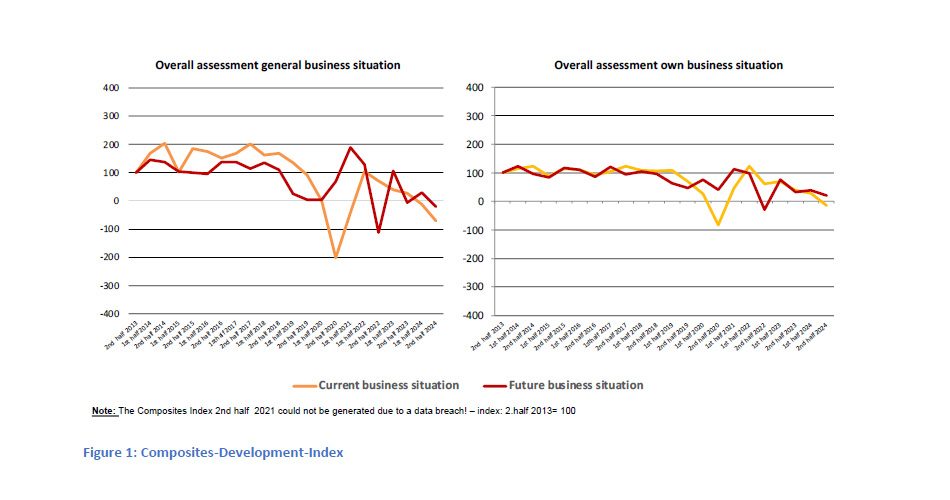

Critical assessment of the current business situation

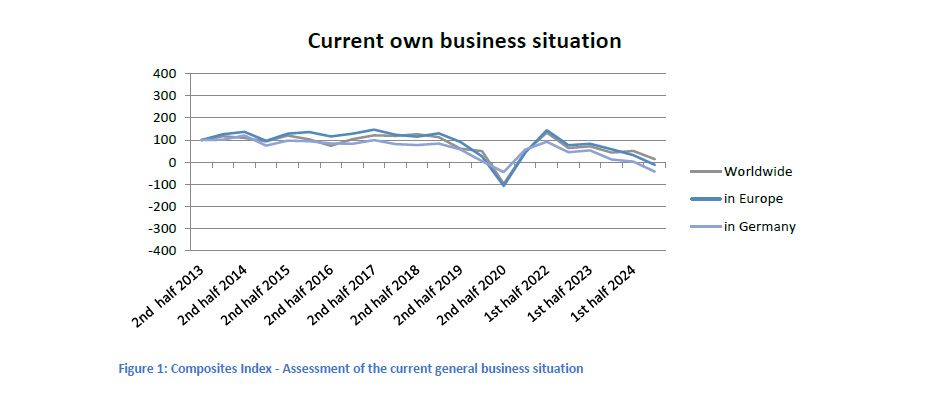

After the assessment of the current business situation was positive at a relatively stable level before the coronavirus crisis, the perception of the survey participants has now deteriorated significantly. With the exception of a few positive trends, the corresponding indicator has been pointing significantly downwards since 2022. There is still no sign of a trend reversal in the current survey. (see Fig. 1). The assessment of the general business situation is declining in all regions mentioned.

The reasons for the negative sentiment are manifold and were already evident in the previous surveys. High energy, raw material and logistics costs remain a major burden, especially for German industry, but also for many other countries in Europe. This is compounded by a weak-ening global economy and weak sales for many products in Asia. Massive competition to Eu-ropean products is growing there, particularly in terms of raw materials, which is also partly

due to overcapacity, which in turn is putting enormous pressure on prices for suppliers here. Political uncertainties, protectionist tendencies and armed conflicts, such as in Ukraine and recently increasingly in the Middle East, are further worsening the economic climate.

At present, politicians do not seem to be succeeding in creating an environment conducive to business. The composites market has already seen sharp declines in the last two years. The industry continues to send pessimistic signals for the current year. The industry was and is an important economic sector for Germany in particular. It is threatened with further decline if the appropriate regulatory framework is not created to enable competitive production. Germany is currently facing structural changes that are necessary, particularly in terms of economic policy and ecology. These necessary adjustments will take many years and require high levels of investment. It is urgently advisable to finally find a balance between the necessary burden on industry/companies on the one hand and corresponding relief on the other. If the decline of German and European industry continues, at some point it will become questionable who should finance the restructuring. Only a healthy economy, which includes a manufacturing industry, will be able to invest and finance the necessary measures.

This will not be possible for the state itself. Even an expansion of employment in the public sector, as has been pushed in recent months to compensate for job losses in industry, only superficially solves this problem. Healthy state financing is based on a healthy economy. Something urgently needs to be done about this – at the moment, we are digging at our own foundations.

It is not only the assessment of the general business situation that remains pessimistic. The situation of their own companies also continues to be viewed critically. The picture is particularly negative for Germany. Almost 70% of respondents are critical of the current business situation in Germany. The view of global business and Europe is somewhat more positive. Here, “only” 46% and 54% of respondents respectively assess the situation rather negatively.

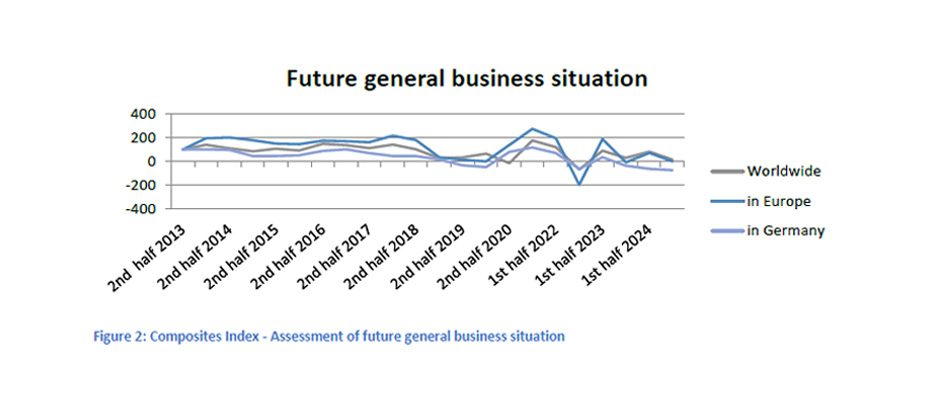

Future expectations are becoming gloomier

While the last survey showed rather positive assessments of future expectations, this picture is currently becoming much gloomier. When asked about their assessment of future business development in general, the figures are consistently negative. At present, the respondents do not seem to believe that the situation will improve. (see Fig. 2).

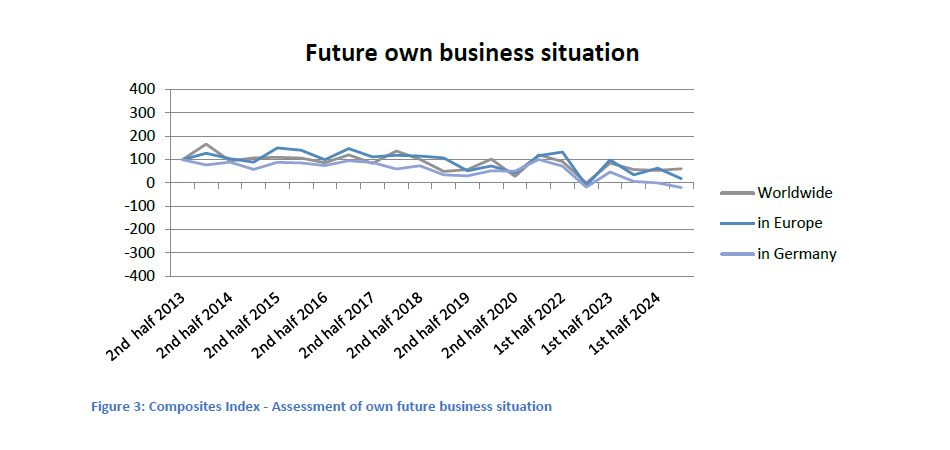

Respondents were also rather pessimistic about their own company’s future expectations, alt-hough their expectations regarding their own market position worldwide were positive (see Fig. 3). It is striking that the view of the German region in relation to Europe and the global economy has been more critical since 2022. 25% of respondents expect the general market situation in Germany to develop negatively. Only 18% expect the current situation to improve. The figures for Europe and the rest of the world are significantly better. Only 3% expect the global situation to deteriorate further. 19% expect the situation to improve.

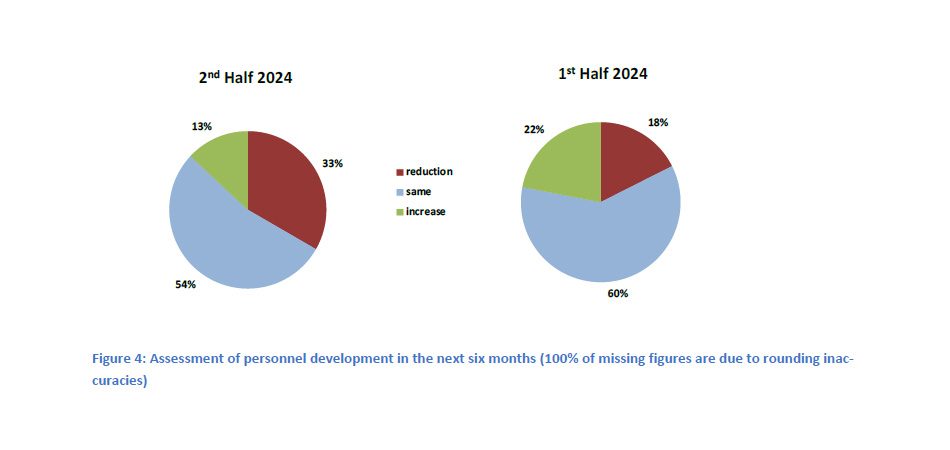

Investment climate remains subdued

The current cautious assessment of the economic situation continues to have an impact on the investment climate. While 22% of participants in the last survey still expected an increase in personnel capacity (survey 1/2023 = 40%), this figure currently stands at just 13%. In contrast, 33% even expect a decrease in the area of personnel (see Fig. 4). The proportion of respondents planning to invest in machinery is also declining. While 56% were still assuming corresponding investments in the last survey, this figure has now fallen to 44%.

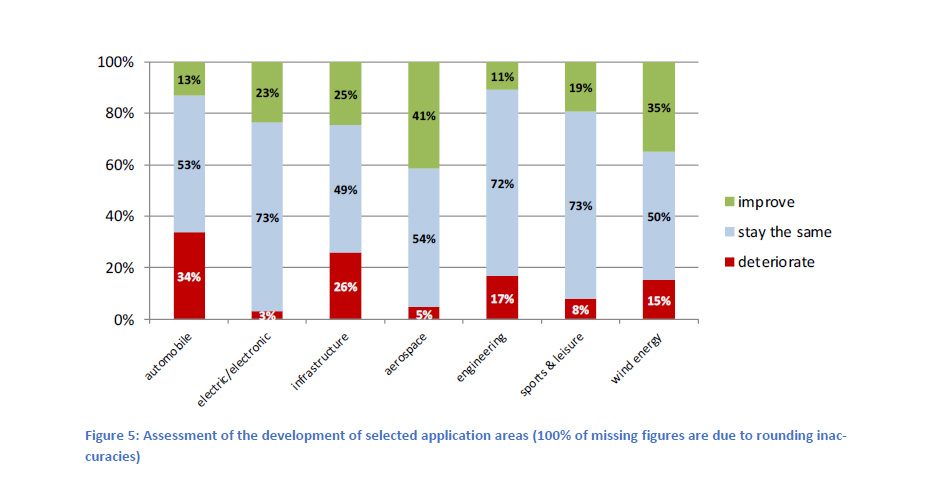

Different expectations of application industries

The composites market is characterized by a high degree of heterogeneity in terms of both materials and applications. In the survey, participants were asked to give their assessment of the market development of different core areas. The expectations are extremely varied. The two most important application areas are the mobility and construction/infrastructure sectors. Both are currently undergoing major upheavals or are affected by declines, which is also clearly reflected in the survey. Growth is expected above all in the wind energy and aviation sectors. (see Fig. 5).

There are generally few shifts here compared to the last survey.

Growth drivers with little movement

In terms of materials, the trend in the assessment of growth drivers is continuing. Whereas for a long time GRP was named as the material from which the main growth impetus for the com-posites sector is to be expected, the main impetus is now once again expected to come from CFRP or across all materials. The trend from the last survey is continuing here. There is a slight regional shift. The main impetus for growth is expected to come from Asia and North America. However, the EU (except Germany) is also mentioned. Germany is seen less strongly as a growth driver and continues to lose ground.

Composites Index points downwards

The numerous negative influences of recent times continue to be reflected in the overall Com-posites Index (see Fig. 6). This is falling in all areas.

In the last two years, the European composites market has lost around 15% of its production volume. Even if not all areas are affected by declines to the same extent, this should be an alarm signal. Until the coronavirus pandemic, there was a continuous increase in production volume for many years. Since the end of the coronavirus crisis and with the increase in macroeconomic uncertainties, Europe and Germany in particular appear to be becoming less attractive as a business location. With production volumes increasing worldwide, Europe’s market share is now steadily declining. There are many reasons for this and there are no simple solutions. However, if the industrial location is to remain secure, something has to change quickly. Once companies have moved away, it is difficult to bring them back.

It remains to be seen whether it will be possible to counteract this negative trend. Targeted intervention, including by political decision-makers, would be desirable here. However, this cannot succeed without industry/business. Only together will it be possible to maintain and strengthen Germany as a business/industry location. For composites as a material group in general, there are still very good opportunities to expand the market position in both new and existing markets due to the special portfolio of properties. However, the dependency on overall economic developments remains.

It is now important to develop new market areas through innovation, to consistently exploit opportunities and to work together to further implement composites in existing markets. This can often be achieved better together than alone. With its excellent network, Composites Germany offers a wide range of opportunities.

The next composites market survey will be published in February 2025.

Press enquiries:

Composites Germany

Dr. Elmar Witten (AVK)

Tel.: +49 69 27107-70,

elmar.witten@composites-germany.org

www.composites-germany.org

About Composites Germany

The two strong organizations of the German lightweight design/composite industry want to strengthen the German composites industry and research, define common positions and safeguard overarching interests with the Composites Germany trade association.

AVK – Industrievereinigung Verstärkte Kunststoffe e. V. and CU – Composites United (as well as VDMA – Arbeitsgemeinschaft Hybride Leichtbau Technologien as an associated partner) are joining forces here with currently over 2,700 active member companies to promote the future topics of high-performance composites and automated production technologies in and for Germany.

Further information at: http://www.composites-germany.org