- Critical assessment of the current business situation

- Future expectations turn negative

- Investment climate cloudy

- Expectations for application industries vary

- Growth drivers with only slight shifts

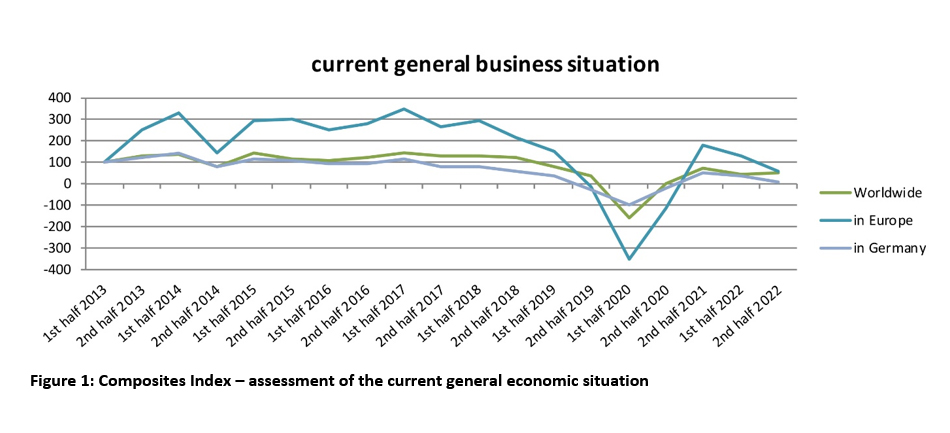

- Composites index points in different directions

This is the 21st time that Composites Germany (www.composites-germany.de) has identified the latest performance indicators for the fibre-reinforced plastics market. The survey covered all the member companies of the umbrella organisations of Composites Germany: AVK and Composites United, as well as the associated partner VDMA.

As before, to ensure a smooth comparison with previous surveys, the questions in this half-yearly survey have been left unchanged. Once again, the data obtained in the survey is largely qualitative and relates to current and future developments in the market.

Critical assessment of current business situation

After consistently positive trends were evident in the assessment of the current business situation in 2021, this slipped in 2022. For the third time in a row, the current survey shows pessimistic assessments (see Fig. 1). The reasons for the negative mood are manifold. However, the main drivers are likely to be the still high energy and commodity prices. In addition, there are still problems in individual areas of the logistics chains as well as a restrained consumer climate. Despite rising registration figures, the automotive industry, the most important application area for composites, has not yet returned to its former volume. This also illustrates the change in strategy of European OEMs to move away from volume models towards high-margin vehicle segments. The construction industry, the second central area of application, is currently in crisis. Although the order books are still well filled in many cases, new orders are often not forthcoming. High interest rates and material costs combined with a high cost of living are placing a heavy burden on private construction in particular. A real decline in turnover of 7% is currently expected for the construction industry in 2023.

The assessment of the business situation of their own company is also increasingly pessimistic. The picture is particularly negative for Germany. Almost 50% of respondents (44%) are critical of the current business situation. The view of global business and Europe is somewhat more positive. Here, “only” 36% and 33% of the respondents respectively assess the situation rather negatively.

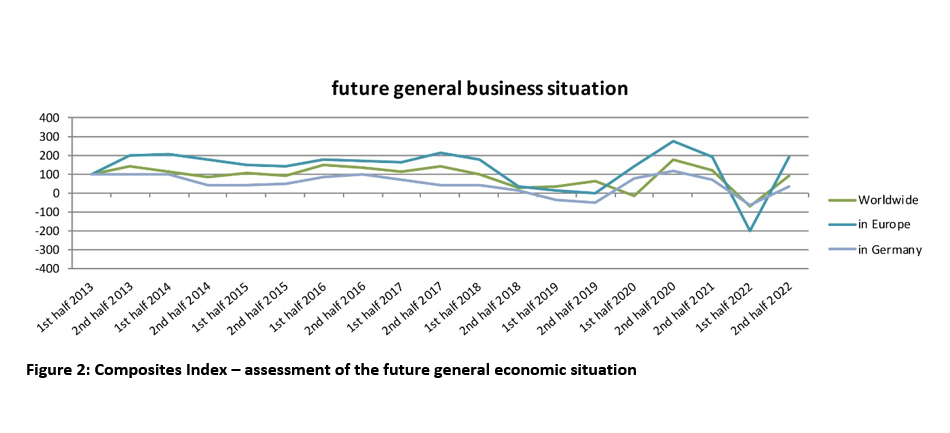

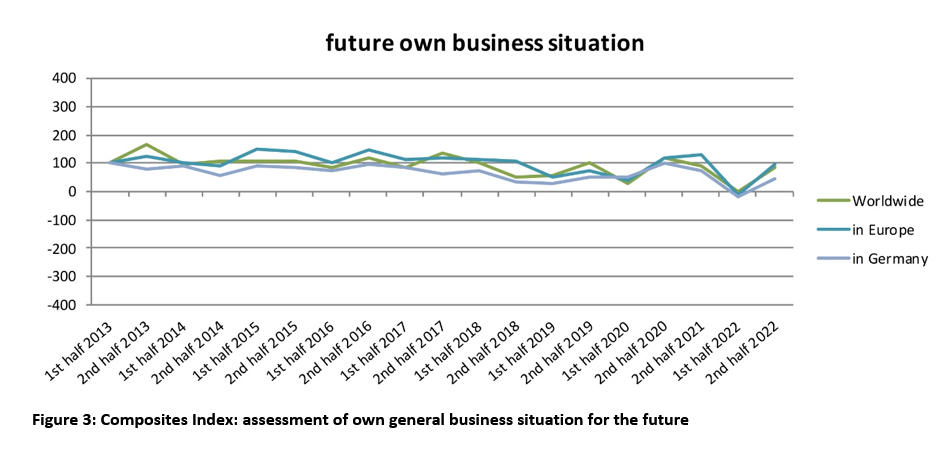

Future expectations turn negative

Following the rather pessimistic assessment of the current business situation, future business expectations also turn negative. After an increase in the last survey, the corresponding indicators for the general business situation are now clearly pointing downwards (see Fig. 2). The respondents are also more pessimistic about their own company’s future expectations (see Fig. 3).

The participants apparently do not expect the situation to improve in the short term. It is also noticeable here that the view of Germany as a region is more critical in relation to Europe and the global economy. 22% of the respondents expect a negative development in Germany. Only 13% expect the current situation to improve. The indicators for Europe and the world are better.

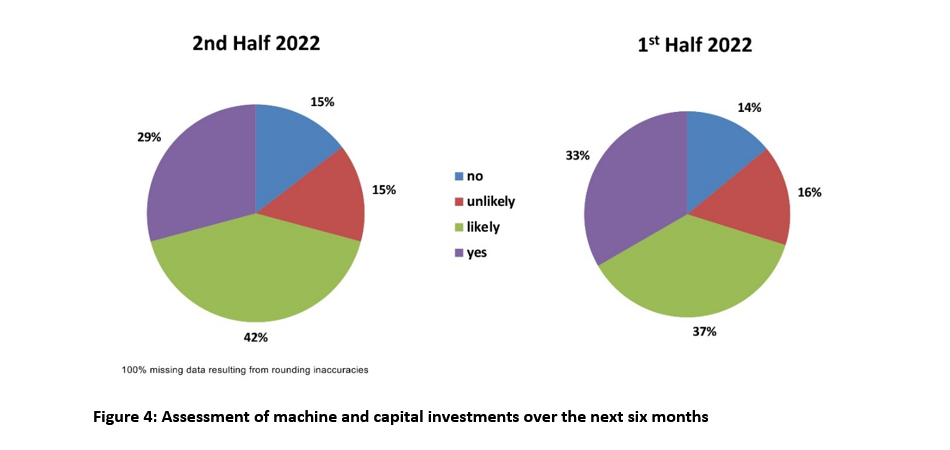

Investment climate clouds over

The currently rather cautious assessment of the economic situation and the pessimistic outlook also have an impact on the investment climate.

Whereas in the last survey 40% of the participants still expected an increase in personnel capacity, this figure is currently only 18%. On the other hand, 12% even expect a decline in the area of personnel.

The share of respondents planning to invest in machinery is also declining. While 71% of respondents in the last survey expected to invest in machinery, this figure has now fallen to 56% (see Fig. 4).

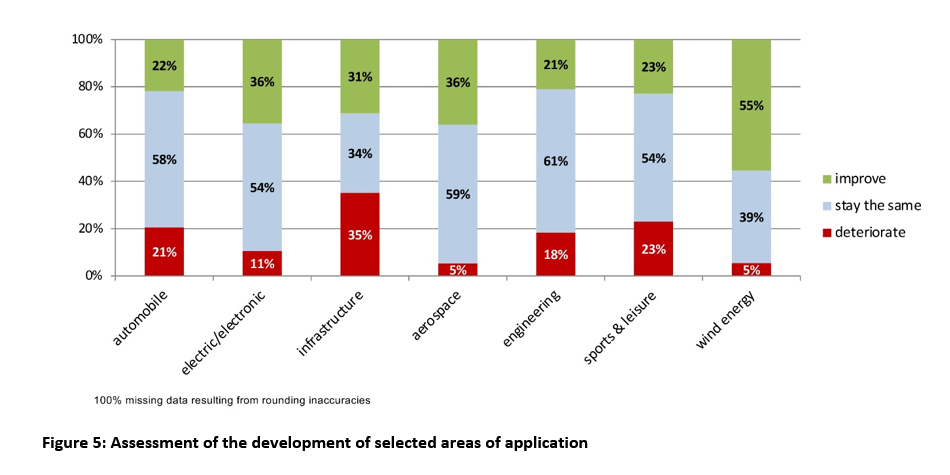

Expectations of application industries differ

The composites market is characterised by strong heterogeneity, both in terms of materials and applications. In the survey, the participants were asked to give their assessment of the market development in different core areas. The expectations are extremely varied (see Fig. 5).

The weaknesses already described in the most important core markets of transport and construction/infrastructure are clearly evident. Growth is expected above all in the wind energy and aviation sectors. Expectations about future market developments, on the other hand, are significantly more positive than the figures presented here might suggest.

Growth drivers with only slight shifts

The paradigm shift in materials continues. While in the first 13 surveys the respondents always named CFRP as the material from which the main growth impulses for the composites sector are to be expected, the main impulses are now assumed to come from GRP or across all materials. There is a slight regional shift. At present it is mainly North America that is expected to provide the main growth impulses for the industry. Europe and Asia are losing ground slightly.

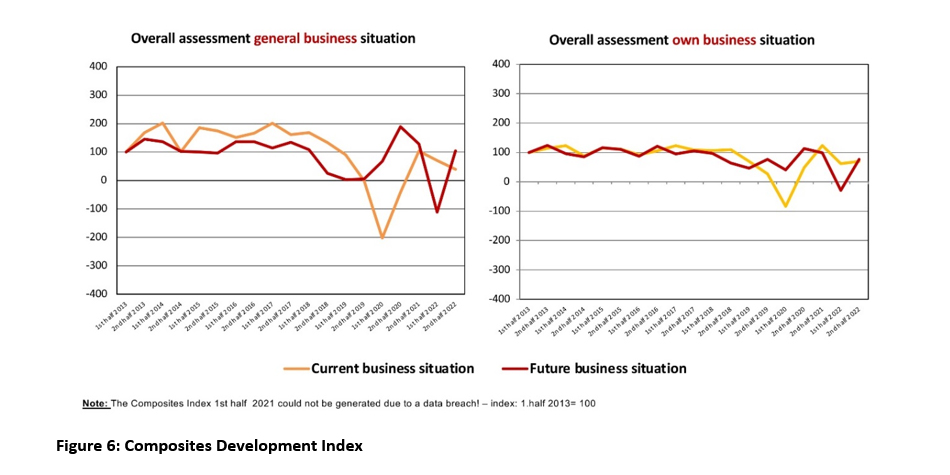

Composites index points in different directions

The numerous negative influences of recent times are now also reflected in the overall composites index (see Fig. 6). All indicators are weakening. Both the current and the future assessment are turning negative.

The total volume of composites processed in Europe in 2022 was already slightly down compared to 2021. After a good first quarter of 2022, there is currently a clear cooling of activity. It remains to be seen whether it will be possible to counteract the negative development. Targeted intervention, including by political decision-makers, would be desirable here. However, this cannot succeed without industry/business. Only together will it be possible to further strengthen Germany’s position as a business location and to maintain or expand its position against the backdrop of a weakening global economy. There are still very good opportunities for composites to expand their market position in new and existing markets. However, the dependence on macroeconomic developments remains. The task now is to open up new market fields through innovations, to consistently exploit opportunities and to work together to further implement composites in existing markets. This can often be done better together than alone. With its excellent network, Composites Germany offers a wide range of opportunities.

The next Composites Market Survey will be published in January 2024.

Press contact:

Composites Germany, Dr. Elmar Witten

Phone: +49 69 92933 401, email: elmar.witten@composites-germany.org

About Composites Germany

With their trade association “Composites Germany”, the three strong organizations in the German lightweight / fiber composite industry want to strengthen the German composite industry particularly in the field of research, determine common positions and take overlapping interests into account.

AVK- Federation of Reinforced Plastics e. V., Composites United and VDMA Working Group Hybrid Lightweight Technologies in the VDMA are bundling their powers to further the future oriented themes high performance composites and automated production technology which are particularly relevant in Germany.

Further information available at: http://www.composites-germany.org