The European composites market 2024 – Market developments, trends, challenges and outlook

Composites market continues downward trend

The European composites industry was unable to halt the downward trend in 2024. European production volumes fell significantly for the third year in a row.

The current trend is largely due to structural weaknesses in key application areas as well as economic and industrial challenges in the core European regions. Germany, which remains the largest economy within the EU, is particularly affected. According to an initial estimate by EUROSTAT, GDP rose by 0.7 % in the eurozone and by 0.8 % in the EU. In the same period, it is estimated to have fallen by 0.2 % in Germany. This negative trend was triggered by general economic weaknesses, particularly in the manufacturing and industrial sectors. The automotive industry and the construction and infrastructure sector in particular, as the most important application industries for the composites industry in Europe, are currently showing strong negative trends.

The picture for the composites industry is similar. The decline in absolute market volume in Europe was coupled with a growing global market. This droves the gap between the European and global composites industry ever wider. Europe’s market share has been declining for many years.

The market under review

The analysis of the AVK considers all glass fibre reinforced (GRP) materials with a thermoset matrix. NCF (non-crimp fabrics) are shown separately. In the thermoplastics market, long fibre reinforced thermoplastics (LFT), glass mat reinforced thermoplastics (GMT) and continuous fibre reinforced thermoplastics (CFRTP) are taken into account. In addition, the European production volume for short glass fibre reinforced thermoplastics is shown separately.

Overall development of the composites market

The volume of the global composites market totalled 13.5 million tonnes in 2024 (source: JEC). In 2023, with a volume of 13 million tonnes, growth was around 4 %. In comparison, the European composites production volume fell by 5.6 % in 2024. The total European composites market thus comprises a volume of 2,416 kilotonnes (kt) after 2,559 kt in 2023. The market is thus declining and falling back to the level of 2012.

Overall, market momentum in Europe was significantly lower than in the global market. Europe’s share of the global market is now around 18 % (after around 20 % in 2023). Market shares continue to shift in favour of America and Asia. As in previous years, the trend within Europe is not uniform. This is due to very different regional core markets, the high variability of the processed materials, a broad spectrum of different manufacturing processes and widely differing areas of application.

In terms of volume, the largest share of total composites production flows into the transport sector, which accounts for almost 50 % of the market volume. The next two largest areas are the electrical/electronics sector and applications in construction and infrastructure.

Development of the market for thermoset composites

The total production volume of thermoset composites (excluding CFRP) amounted to 983 kt in 2024, compared to 1,073 kt in the previous year. This material group therefore accounted for 41.8 % of the total market in Europe. Compared to the long-term trend, there is now a clear decline market share in contrast to thermoplastic systems. The main areas of application for thermoset composites remain the construction/infrastructure sector and the transport sector

Development of the market for thermoplastic composites

The market for thermoplastic composites in Europe had a total volume of 1,368 kilotonnes (kt) in 2024, compared to 1,423 kt in the previous year. Nevertheless, the market share of these systems in the overall European market rose to 58.2 % after 57 % in 2023. Compared to the previous year, the market volume fell by 3.9 % and thus less significantly than for thermoset materials. The largest material group within thermoplastic composites, but also in the overall market, are the so-called short glass fibre reinforced plastics. The second largest group within the group of thermoplastic materials are long fibre reinforced plastics (LFT). The main area of application for thermoplastic composites is the transport sector, which accounts for almost two thirds of the market. Within this segment, the passenger car and commercial vehicle sectors dominate. Together with electrical/electronic applications, this results in a market share of almost 90 % by 2024. The passenger car market is of central importance for thermoplastic composites. While there was often talk of economic weakness in the automotive industry in the first two years after the coronavirus pandemic, the full extent of the structural problem in the European and, above all, German automotive industry will be revealed in 2024. There is also a general trend on the part of European OEMs (original equipment manufacturers), which continues to depress sales figures. The vehicle market is showing signs of recovery, but this is currently only reflected in the European composites market to a very limited extent.

Trend developments in processes/parts

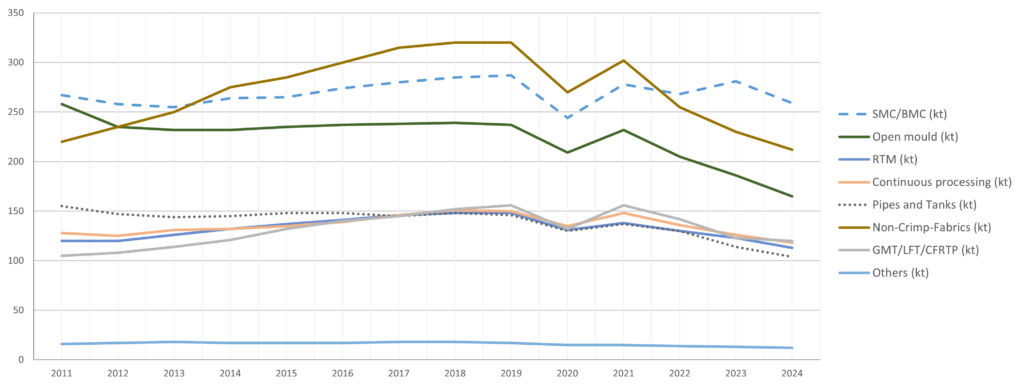

SMC/BMC, the largest single segment in the European GRP market (all thermoset as well as long and continuous fibre-reinforced thermoplastic materials) with a market volume of 259 kt, recorded a drop in production volume of almost 8 % in 2024. Reasons for this include regulatory uncertainties in specific application areas and slower demand in the automotive, construction and infrastructure sectors. The SMC market will decline by 7.4 % and the BMC market by 8.9 % in 2024.

NCF, the second largest group, still has a volume of 212 kt, with the market segment losing 7.8 % overall. Despite high investments in wind energy, the segment remains under pressure as production is increasingly dominated by Asian suppliers.

Open processes – hand lay-up and fibre spraying – continue to be one of the largest segments in the GRP market in Europe with a production volume of 165 kt. In 2024, however, this market segment also declined by an above-average 11.3 % – due to stricter legal requirements, a shortage of skilled labour and declining demand in special application areas.

After a phase in which RTM processes were able to develop continuously, the European production volume fell by 8.1 % to a total of 113 kt. This means that the decline is roughly as high as that of the entire thermoset composites market.

The production of GRP components using the so-called continuous processes (pultrusion and production of flat sheets) will see a 6.4 % decline in volume in 2024. Overall, the production level for pultrusion will fall by 4 % to a volume of 48 kt. For flat sheets, there will be a decline of 7.9 % to a volume of 70 kilotonnes.

The market segment of GRP pipes and tanks, manufactured using centrifugal or winding processes, fell by 6.3 % in the year under review. The production volume totalled 104 kt in 2024, with 56 kt attributable to the winding process and 48 kt to the centrifugal process. Despite a generally positive outlook for the future, this sector is also particularly affected by the weaknesses in the construction and infrastructure sectors and the difficult economic situation.

The market for GMT declined by 4.3 % to a total volume of 22 kt in 2024. The decline was therefore slightly higher than that of the overall market for thermoplastic materials, which shrank by 3.9 %. LFT (long fibre reinforced thermoplastics) lost 2.2 % overall in 2024, reaching a production volume of 88,000 tonnes. CFRTP (continuous fibre-reinforced thermoplastics) remain a niche product. There were no significant changes here, which should be seen as a positive sign against the backdrop of a generally declining market. The market segment reaches a volume of 10 kt.

Even though the properties of short glass fibre-reinforced materials sometimes differ significantly from those of long and continuous fibre-reinforced systems, this important group of materials is classified as composites. The European market for thermoplastic short glass fibre reinforced materials will decline by almost 4 % in 2024. The production level will fall to 1,248 k. Nevertheless, short glass fibre reinforced thermoplastics remain by far the largest single segment in the composites industry.

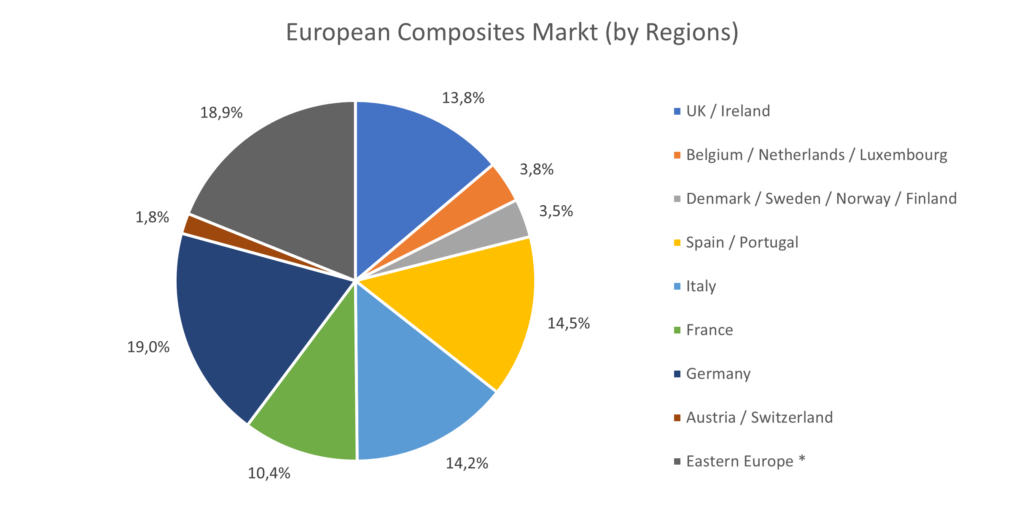

Regional market development

The percentage shifts by regional focus only changed in 2024 compared to 2023 in the post-comma area. Overall, there were absolute declines in all regions surveyed.

The German thermoset market will reach a volume of 187 kt in 2024 (2023 = 208 kt). With a share of 19 %, Germany is once again currently the largest market within the regions covered. The Eastern European countries follow in second place with a market share of 18.9 %. This region includes Poland, the Czech Republic, Hungary, Romania, Serbia, Croatia, Macedonia, Latvia, Lithuania, Slovakia and Slovenia. Spain/Portugal is the third largest group with a market share of 14.5 %. Italy follows just behind with a market share of 14.2 %. Together, these four regions account for almost two thirds of the European composites market. The next largest processing region is the UK/Ireland with a market share of 13.8 %. France is well behind with a market share of 10.4 %. The remaining processing regions are led by the Benelux countries with a share of

3.8 %. The volume was slightly lower in the Northern European countries at 3.5 %. Austria/Switzerland accounted for the lowest percentage share at 1.8 %.

It is important to bear in mind that the composites industry has very different centres of gravity in almost all regions. Accordingly, the various countries/regions are often affected very differently by macroeconomic developments.

Comment: The European (composites) industry is at a crossroads – An appeal to value creation

“If you realise, you’re riding a dead horse, get off!”

This metaphor can be applied to the current discussion about the future of industry in Europe. Key indicators, such as the crisis in the automotive industry, weakening construction activity and rising energy prices, point to a difficult situation. At the same time, production in emerging economies such as China and India is increasing, while the competitiveness of established industries is declining

So, is it time to get off the horse? Is the European (composites) industry really at the end of the road and will it ultimately have to bow to the fact that production can be better and cheaper in other regions? From the point of view of the European composites industry, this is the wrong way to go!

Europe is going through a period of profound upheaval, but this does not mean the end. The upheaval will not be quick or easy, but it is necessary to ensure competitiveness. A simple “business as usual!” will not be enough. The question is one of medium-term solutions and what has characterised our industry for decades – quality, innovative strength and research.

Europe cannot compete globally with low-price models, especially not with China. But instead of writing off the industry, it should seize new opportunities. The debate on sustainability offers potential for the composites industry in particular, as new drive systems and renewable energies offer great potential for growth. These opportunities must be promoted through political support and a fair international competitive environment.

Sustainable structural change is necessary to combat climate change. It is crucial that Europe pushes ahead with its innovations. Research cooperation and investment in new technologies such as AI and robotics are essential. European industry must expand its innovative strength and at the same time optimise the value chain, from the idea to the finished product.

The current crisis is not just a consequence of the coronavirus pandemic, but the result of long-term problems. The industry must act decisively now in order to reposition itself in the medium and long term.

The composites industry has great potential, especially in times when new challenges also bring new opportunities. The European industry is not finished – it just needs to find new ways to move successfully into the future – then the horse can continue to be ridden.

AVK’s Market Report for Fibre Reinforced Plastics / Composites 2024 highlights developments, trends and challenges and looks to the future. You can find the entire Market Report 2024 on AVK website at www.avk-tv.de. This press release is an abridged version of the report.